This question cuts to the heart of “your money or your life” where the opposing forces of dignified old age vs financial security dictate that the longer you live, the less likely you can afford it.

Sure, there’s the lucky few who earn enough annually from retirement savings that they don’t eat into their capital, but for the majority of retirees (generally age pensioners) there’s a reasonable chance that significant assets (such as a home) would need to be sold to meet ‘later in life’ expenses such as aged care, medical needs etc etc.

Simply put, the age pension is not enough for single or couples to maintain a modest retirement and certainly not enough to meet all the possible health challenges later in life. In fact the Association for Superannuation Funds of Australia (ASFA) publish their financial standards which, for a modest retirement, would require someone to always have a spare pool of retirement assets (usually super or cash savings)

So have you given much thought to how long you could last?

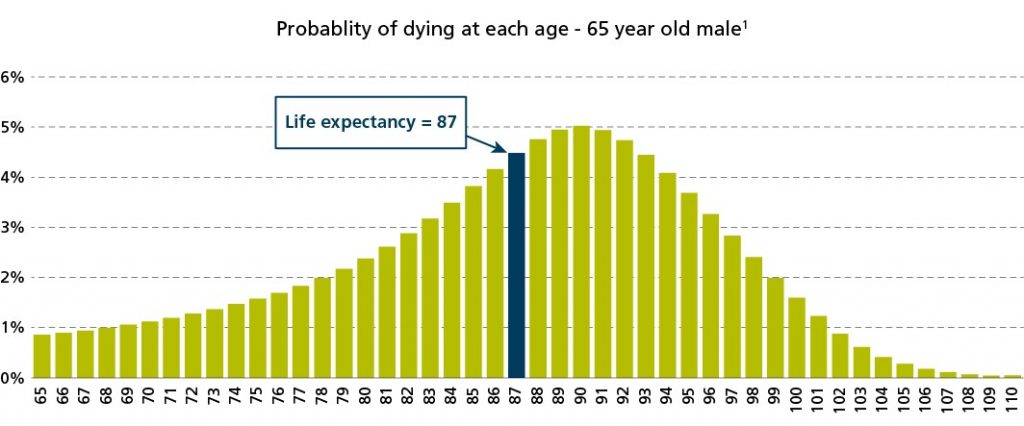

One limitation to longevity statistics is this false sense of security that we’ll hopefully get to our life expectancy and ideally a few years past but what if it’s a few too many years past? As the numbers show, there’s actually about the same chance a 65 year old male will die in that first year, as the chance they’ll die at 102. That’s a big age range!

Source: Challenger, May 2021

One of the most satisfying elements of my work life is to help people make good choices, not just with their money, but to meet their life goals. Some retirees have technical goals like “I don’t want to pay tax” or “I want to maximise my investment returns” but sometimes the more subjective goals like “I want my money to outlast me” should take priority. The earlier a person addresses that goal in retirement (actually ideally pre-retirement), the better the chance they have of managing longevity risk.

When helping our clients, it includes clarifying the consequences of decisions that are made throughout retirement: Should I buy a caravan? Have I got enough to go to overseas? I’m thinking about putting solar on the roof… It’s not for me to dictate how much you will enjoy a trip to Fiji, or the satisfaction of opening a $0 power bill, but we can measure what it means to your retirement pool of assets over the long term. We do this by calculating projections and rather than stopping clients from spending money, it often actually liberates the decision making because the consequences are more defined which then lead to more specific goals.

For instance: Should I buy a caravan? Yes, absolutely, but by doing so let’s focus on other areas of expense in the future to minimise the risks of outliving your money…

The key is to seriously consider your longevity risk, understand what you can do about it and make some good decisions to preventatively manage those risks earlier in retirement. We’re here to fill in the details about how to make those good decisions, so call us in need.