Treasurer Jim Chalmers has proposed that from 1 July 2025, taxation on earnings from superannuation balances above $3 million will double to 30%.

The new policy is expected to raise about $2 billion a year.

As always, the devil is in the detail. Initially framed as a simple increase to the existing 15% tax on super fund earnings, the Treasury Consultation Paper makes it clear that this is unequivocally a new tax and will be levied against individuals in a similar way to Div. 293 tax levied on super contributions for higher income earners.

The Key Details

- Proposed to start from 1 July 2025, after the next Federal Election.

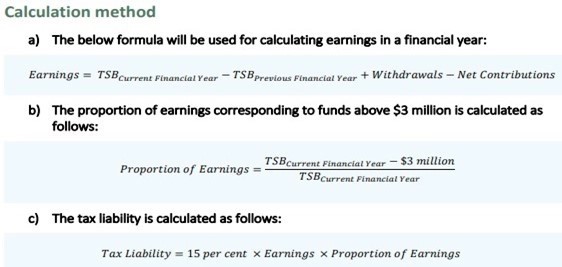

- Contrary to the Treasurer’s press release, this is a new tax and will be calculated differently from the existing 15% tax on superannuation earnings.

- The new measures are proposed to tax increases in a member’s Total Superannuation Balance (TSB), effectively taxing capital gains, whether realised or not.

- The 33.33% discount on capital gains (for assets held more than 12 months) will not apply to this measure. Capital gains will be taxed twice; once at 15% on the annual movement in asset values, and a second time at 15% or 10% upon disposal.

- For SMSFs with limited recourse borrowing arrangements (LBRAs) where the loans were from an associate, or maintained after a condition of release is met, the LRBA will not reduce the TSB. The gross value of the assets will count toward the TSB. LRBAs may need restructuring before 1 July 2025.

- The tax can be paid from outside superannuation, or the member can elect to have it paid from the fund (similar to division 293).

- It is still not clear how this will impact members of defined benefit schemes (including politicians and public servants).

- The $3 million limit is not intended to be indexed, which will greatly increase the number of payers in future years.

No Indexation

One of the concerns is that indexation won’t apply to the $3 million threshold. Bracket creep will capture an increasing number of super fund members over time.

It’s also possible that future Governments may seek to lower the $3m threshold, once implemented. For example, Div. 293 tax was introduced in July 2012 for taxpayers with income over $300,000. In July 2017 that threshold was reduced to $250,000 and no indexation upwards has been applied.

Unrealised Capital Gains

A tax on unrealised capital gains could be problematic for those with illiquid assets in their super fund, such as small businesses and farming families. Under existing rules, superannuation capital gains are only taxed when an asset is sold within the fund. This new proposal would effectively tax the assets of the fund on their capital gains before they are sold.

Examples

Treasury’s example of a balance exceeding $3 million

Warren is 52 with $4 million in superannuation at 30 June 2025. He makes no contributions or withdrawals. By 30 June 2026 his balance has grown to $4.5 million.

- Warren’s calculated earnings are $4.5 million – $4 million = $500,000.

- His proportion of earnings corresponding to funds above $3 million is ($4.5 million – $3 million) ÷ $4.5 million = 33%

- His tax liability for 2025-26 is 15% × $500,000 × 33% = $24,750

Note that this is extra tax, an additional amount above the tax that Warren would currently pay.

Treasury’s example of the earnings calculation

Carlos is 69 and retired. His SMSF has a superannuation balance of $9 million on 30 June 2025, which grows to $10 million on 30 June 2026. He draws down $150,000 during the year and makes no additional contributions to the fund.

- Carlos’s calculated earnings are: $10 million – $9 million + $150,000 = $1.15 million

- His proportion of earnings corresponding to funds above $3 million is ($10 million – $3 million) ÷ $10 million = 70%

- Therefore, his tax liability for 2025-26 is 15% × $1.15 million × 70% = $120,750

Treasury example of a carry-forward loss

Dave is 70 and has two APRA-regulated funds and one SMSF. At 30 June 2025, his TSB across all funds was $7 million. During 2025-26, he withdraws $400,000 from his SMSF and makes no contributions. At 30 June 2026, his TSB across all funds is $6 million.

- This means Dave’s calculated earnings are $6 million – $7 million + $400,000 = minus $600,000.

- His proportion of earnings corresponding to funds above $3 million is ($6 million – $3 million) ÷ $3 million = 50%.

- The earnings loss attributable to the excess balance is $300,000. Dave can carry forward the $300,000 to offset future excess balance earnings.

At 30 June 2027, Dave’s funds make earnings on his excess superannuation balance of $650,000. He carries forward the earnings losses attributable to his excess balance at 30 June 2026 of $300,000 and is only liable to pay the tax on $350,000 of earnings.

- This means his tax liability for 2026-27 is 15% × $350,000 = $52,000.