Home | Newsletters | Goldsborough News – April 2026: Aged Care, Age Pension and the Family Home

Goldsborough News – April 2026: Aged Care, Age Pension and the Family Home

Aged Care, Age Pension and the Family Home

2-Year Exemption

When a single person moves into residential aged care and the home is not occupied by a spouse, the home is an exempt asset for aged pension calculations for up to 2 years from the time the home is vacated (i.e. time of entering permanent care). They retain “homeowner” status during the 2-year exemption period.

At the end of this period, the home is fully assessable under the assets test for age pension calculations, and the person is then assessed as a “non-homeowner”. Given the values of residential real estate, a significant reduction or loss of age pension altogether is likely.

If a protected person (other than a spouse) remains in the home, the 2-year exemption only applies for age pension calculations (but may qualify for an exemption when calculating aged care fees).

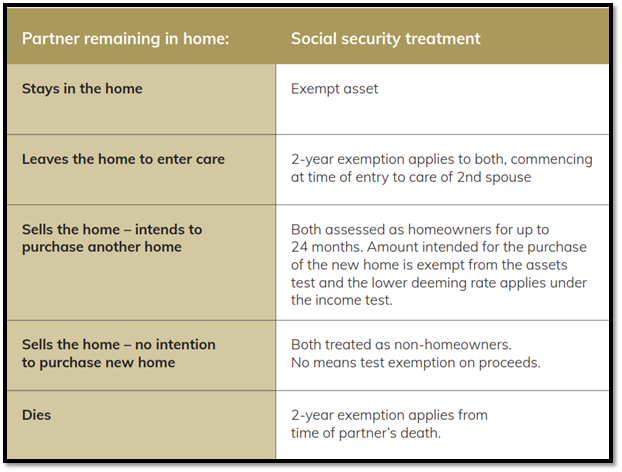

Spouse remains in home

When one member of a couple enters care, the home continues to be an exempt asset whilst the spouse remains at home. If the spouse sells the home and buys another home and moves in, it will continue to be exempt from assessment. However, if there are any residual funds from the changeover, those funds will be assessed for both age pension and aged care calculations.